.1)[1].2007151419286.jpg)

A person wanting to start a new business often wonders what is the first step. Once you have your idea it's hard for new business owners to determine how they want to structure their new business. These are the three main categories of companies. These different types of companies will determine the amount of risk or liability you have, how much you can gain from the business and what you pay in taxes. This article is an overview of the different types of businesses, however, it is not a complete list of all the different types of business entities. This article is geared towards new business owners. These different business structures can help you structure the perfect business for you and your dream.In Florida, the business structures are governed by Fla. Stat. Ann. tit. XXXVI § 605-623 (2019).

Sole Proprietorship

The first type of business structure is a Sole Proprietorship. It is the simplest and most common business structure. A sole proprietorship is an unincorporated business operated by one individual. Becoming a sole proprietorship will give you complete control of your business. This means that you are inevitably the sole proprietor for the activities of the business, even if you don’t register as any other type of business. With this type of structure, your business assets and liabilities are not separate from any of your personal assets and liabilities. You can be held liable for any debts or obligations of the business. A positive of becoming a sole proprietor is it is easy to get started. The paperwork is limited which makes it perfect for owners who want to test out the idea and success of a business. In Florida, a sole proprietorship does not have to register with the Florida Secretary of State or go through any other legal formalities. Unless the business owner does not want to operate their sole proprietorship under their own legal name. Sole proprietorships that are not operating under the owner’s legal name must register a fictitious name with the Division of Corporations. Furthermore,

Partnerships

Partnerships are for people who want to start a business with another person or partner. There are multiple different types of partnerships. Fla. Stat. Ann. tit. XXXVI § 620 (2019) controls the formation of a partnership. The different types of partnership affects how much liability a partner has to the business. When determining if the type of partnership you want it is important to keep three things in mind. Who do you want to have the authority to make decisions? How are the profits and losses going to be divided up? Lastly, how does the government regulatory scheme impact your business entity?

General Partnership: a general partnership is appealing to business owners because it is easy to create. First, there is no required written agreement. There only needs to be a specified mutual manifestation of consent. This means the partners need to just agree and consent to creating a partnership. Second, there are no registration requirements. You just need to start doing business together. In a general partnership there is an equal sharing of ownership and management functions. Therefore, each partner has full and equal right to participate in the management of the business. There is also unlimited personal liability in a general partnership. This means all partners are jointly and severally liable for all obligations of the partnership. There is also no limit to potential personal liability. Furthermore, each partner owes a fiduciary duty to act fairly and honestly to the other partners. Another thing to keep in mind is that the individual partner’s adaptability to changed circumstances is favored over the company’s continuity and adaptability. This means if a partner wishes to dissolve the partnership they can do so at any time if they pay the expelled partner the value of their interest in cash. A general partnership is very adaptable however this can lead to a lack of stability.

Joint Venture: A joint venture occurs when partners join together for a limited business purpose. A joint venture is less permanent. Furthermore, there is less merging of assets and interests. This type of partnership is great for business with a limited purpose. Joint ventures do not require a contract in writing. However, it is often better to get an agreement in writing because it could possibly be deemed a general partnership. In a joint venture the partners have an equal right to a voice in the direction and control of the group and a right to share in the profits and a duty to share in any losses.

Limited Partnerships (LP): An LP is a business association composed of one or more general partners and one or more limited partners. LP’s are formed by filing a certificate of limited partnership with the secretary of state. The Florida Revised Uniform Limited Partnership Act of 2005 governs limited partnerships. It can be found at Fla. Stat. Ann. tit. XXXVI § 620 (2019) . This partnership is optimal for a business that wants to separate ownership and management functions. The general partner or partners participate equally in management and decision making while also being agents of the business. The limited partners have no management power and no authority to act as agents of the business. However, if limited partners participate in the management and decision making they risk becoming a general partner. Limited partners will need to watch out for this because general partners can be held jointly and severally liable for the partnership. Normally, limited partners are not personally liable for limited partnership’s obligations.

Limited Liability Partnerships (LLP): A LLP allows every partner to participate in the management and decision making of the company, while limiting their personal liability. A LLP operates similarly to a general partnership, however, only the partnership itself is liable. To create a LLP, it must be registered with the state. LLPs are more flexible in allowing partners to leave without dissolving the partnership. This creates more stability in the partnership.

Limited Liability Limited Partnership (LLLP): A LLLP is very similar to a limited partnership because there are both general and limited partners. However, a LLLP must be registered with the state in order for all partners to have no personal liability.

This link will take you to the appropriate forms to fill out when forming a partnership.

Corporations

A corporation is a company authorized to act as a single entity. This means a corporation is a legal entity separate from its owners. Therefore, corporations can enter into contracts, own assets, loan and borrow money, pay taxes, be held liable and hire employees, just like a person. Corporations are governed by Fla. Stat. Ann. tit. XXXVI § 607 (2019) . A corporation has shareholders, directors and officers. Shareholders provide capital contributions and they do not have any management functions. Directors make the major policy decisions and are considered an agent of the corporation. However, directors must act as a board to work as an agent of the corporation. Officers provide the day to day management of the corporation and are employees of the corporate. A corporation is created by a group of shareholders, holding common stock, incorporating the corporation. Furthermore, to create a corporation you will need to file an articles of incorporation with the state and then issue stock to the shareholders. The articles of incorporation creates the corporation and contains the external files of the corporation. Corporations are taxed twice, once when the company makes a profit, and another when dividends are paid to shareholders. They can also raise capital through raising funds of the sales of stock, and that can attract employees.

This link will take you to the appropriate forms to fill out when forming a corporation.

Limited Liability Company

Developing a Limited Liability Company (LLC) is a combination with benefits from a corporation and partnership. LLCs are not incorporated but must be filed with the secretary of state. Furthermore, LLCs are contract based. This means you must have a contract to form one. Limited liability companies are governed by Fla. Stat. Ann. tit. XXXVI § 605 (2019). LLCs can elect whether they want to be treated as a corporation or as a partnership for tax purposes. This makes it a very desirable business structure. Structuring an LLC will protect yourself and your personal liabilities and assets. If you have to place your LLC into Bankruptcy or a lawsuit, your personal liabilities and assets are protected. LLC’s are structured for medium to high-risk businesses. They are also beneficial to someone with significant personal assets and someone that wants to pay lower tax rates. If you opt to develop an LLC, then you are considered self-employed and must pay self-employment taxes, pay into Social Security and Medicare. You can avoid corporate taxes by passing profits and losses through your personal income. Unlike a corporation, there are managers instead of directors and members instead of shareholders. Furthermore, there are almost no immutable rules. However, the operating agreement and contract allows for modification. However, you cannot modify to get rid of the duty of loyalty and duty of good faith.

Professional Limited Liability Company (PLLC): is a subgroup of an LLC. With a PLLC, these businesses are formatted with a license to be established as a professional. Examples of PLLC’s often include law firms, architects, chiropractors and accountant firms, for example, will start a PLLC due to the need of a license. A PLLC member is protected from individual liability from their liability with the business.

This link will take you to the appropriate forms to fill out when forming a limited liability company.

Tax Designations

There are multiple different types of tax designations pertaining to corporations. One to keep in mind is a tax designation called: S-Corporation. The S-Corporation, or S-corp, is designed to avoid the double taxation from C-corps. They allow profits and losses to be passed through the owner’s personal income while avoiding the corporate tax rates. Some states tax the S-corps differently, but most are taxed like the federal government would tax. They must file with the IRS to get S-corp stats. One difference with an S-corp is they limit at 100 shareholders, which all must be US citizens. A shareholder can sell or leave the company, and the business can function as usual. S-Corporation is for corporations that meet the specific Internal Revenue Code requirements. However, it gives corporations with 100 shareholders or less the benefit of being incorporated while also being taxed as a partnership. Furthermore, S-corporation is not only for corporations, LLCs can also use this tax designations. In order for a business to become a S corporation, the corporation must submit Form 2553 Election by a Small Business Corporation. We will Link the application and more resources below.

Another tax designation to keep in mind is the B-Corporation. The B-corp, or benefit corporation, is recognized by the United States as a for-profit corporation. One of the common features from the other corporations is the way they are taxed. An advantage from developing this type of corporation is that it is driven by mission and profit, and some states require an annual benefit report for their impact on the good of the public. Shareholders also hold the company accountable for the public benefit and financial profit.

Thing to Keep in Mind

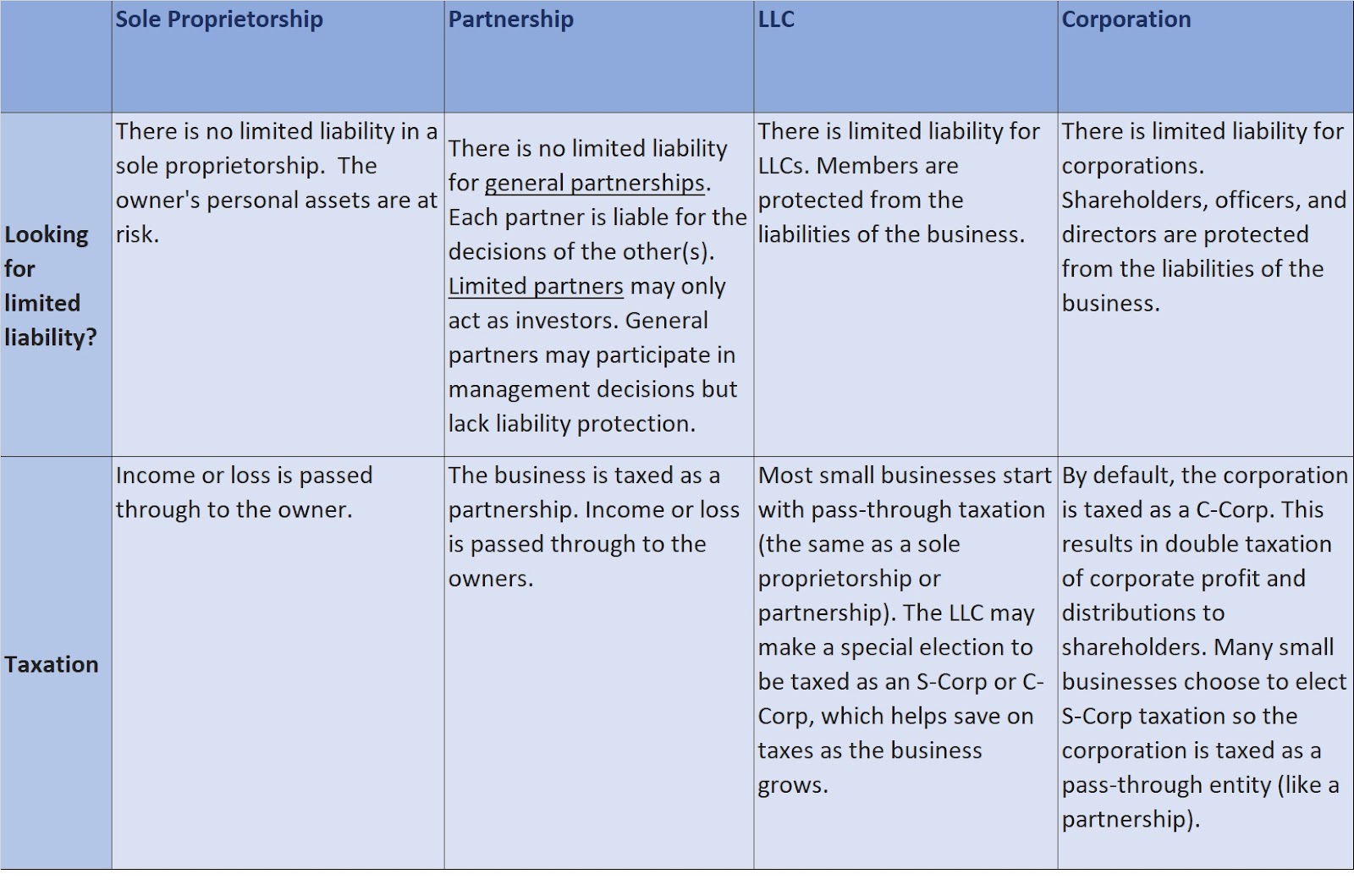

When determining what business structure is right for your business, it is important to determine the amount of liability that you want. Personal liability can be a major deterrent from some of the business structures, like a general partnership or joint venture. When a partner is personally liable, creditors can go after the partner’s personal assets. Furthermore, if a business owner wants to limit who can manage their business they will want to steer clear from a general partnership or joint venture. Limited liability is a type of legal structure for a business entity where a corporate loss does not exceed the amount invested in the business. Furthermore, businesses tend to want to avoid double taxation. Therefore, new business owners tend to lean towards business structures with pass-through taxation treatment. Pass-through taxation means the taxes of a business are passed through to the tax returns of the individuals who own the business which means they are not subject to double taxation. Here we have created a chart that will help you keep track of the liability and taxation associated with each business structure.

Once you have determined who you want to have authority, and liability you will be on your way to determining a business structure that is right for you. Under additional resources we have linked Sunbiz.org. Sunbiz is Florida’s website that provides all the forms to form your business. We have linked their step by step process to file the appropriate forms to form your new business.

Additional Resources